Student Loan Collections: A Deep Dive into Trump’s Policies

By Darius Spearman (africanelements)

Support African Elements at patreon.com/africanelements and hear recent news in a single playlist. Additionally, you can gain early access to ad-free video content.

The landscape of student loan repayment in the United States has undergone significant shifts, particularly impacting millions of Americans, including a disproportionate number of Black borrowers. The Trump administration has taken decisive action to restart collection efforts on defaulted federal student loans. This includes measures such as wage and federal benefit garnishment (businessinsider.com).

This move marks a significant departure from the previous pause in collection activities. It carries profound implications for the financial well-being of individuals and families across the nation. For many, especially those from marginalized communities, these policies add another layer of economic strain. They highlight the ongoing struggle for financial stability and upward mobility. Understanding these changes is crucial for anyone navigating the complexities of student debt.

The Return of Collections: A Harsh Reality for Borrowers

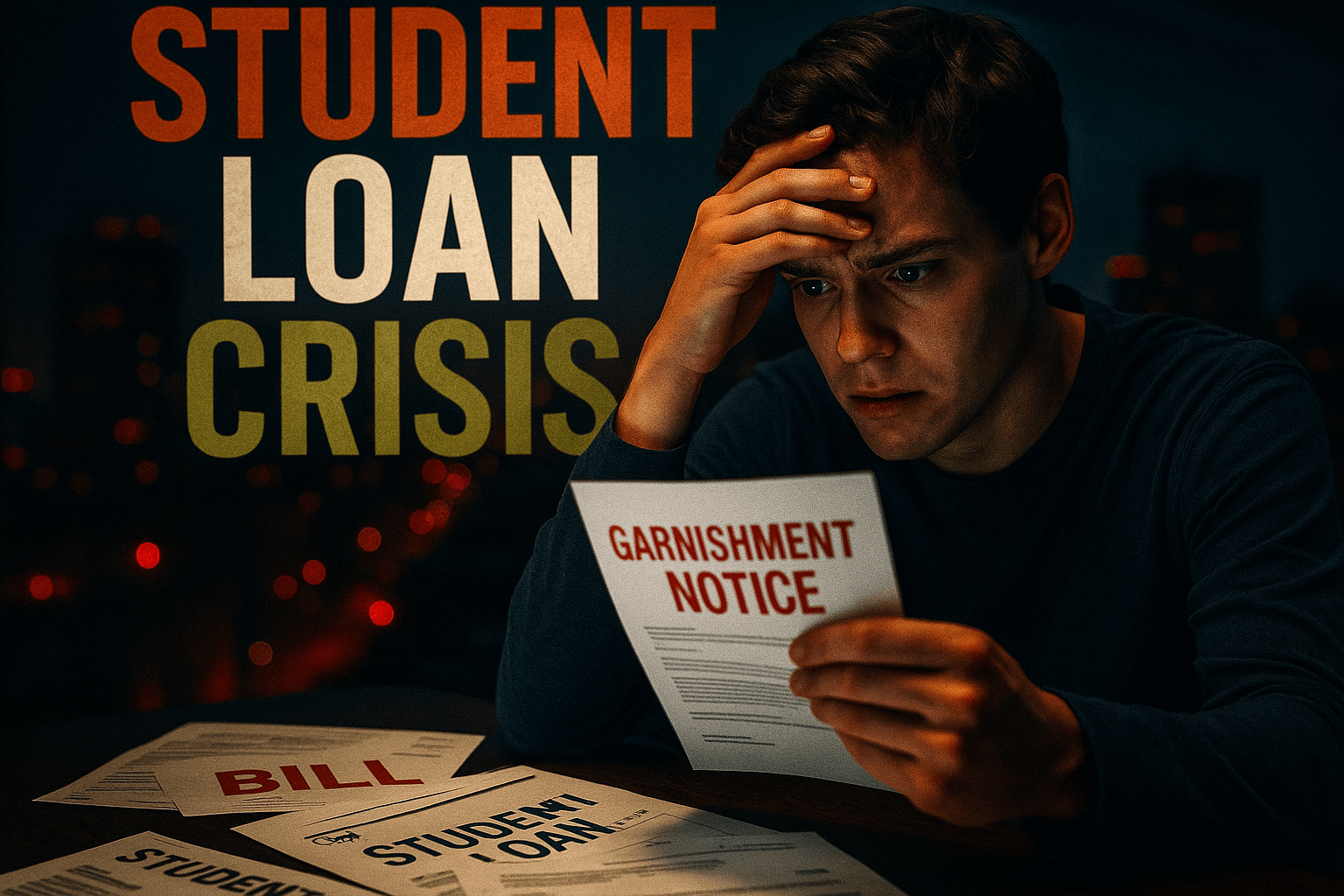

The Trump administration officially restarted involuntary collections on defaulted student loan borrowers’ debt on May 5 (businessinsider.com). This means that individuals who have failed to make payments on their federal student loans according to the agreed-upon terms are now facing serious consequences. A defaulted loan occurs when a borrower fails to make payments on their loan according to the agreed-upon terms. Delinquency is the initial stage of missed payments. Default, however, signifies a more prolonged failure to repay, often leading to more severe consequences (bidenwhitehouse.archives.gov).

The U.S. Department of Education announced plans to garnish wages and federal benefits, including Social Security retirement checks, for defaulted borrowers (newsone.com). Wage garnishment is a legal procedure. A portion of an individual’s earnings is withheld by an employer and sent directly to a creditor to satisfy a debt. Similarly, federal benefit garnishment involves the withholding of federal payments, such as Social Security, to repay outstanding debts (desifacts.org). The legal basis for these actions typically stems from court orders or specific federal statutes that allow for the collection of certain debts. Approximately 195,000 student loan borrowers have already been alerted that their federal benefits could be garnished within 30 days (newsone.com).

The Treasury Department will send notices to 5.3 million defaulted borrowers regarding wage collection activity “later this summer” (cnbc.com). This widespread action will undoubtedly impact millions of households. Delinquencies and defaults on student loans can significantly lower a borrower’s credit score. A credit score is a numerical representation of an individual’s creditworthiness, based on their credit history. A lower credit score can negatively impact a borrower’s financial life. It makes it more difficult and expensive to obtain future loans, such as mortgages or car loans. It can also affect the ability to rent an apartment, get certain jobs, or even secure lower insurance premiums (urban.org). The Federal Reserve Bank of New York reported that 2.2 million student loan recipients saw their credit score drop by at least 100 points. Another 1 million saw their scores drop by over 150 points as a result of these collection efforts.

Scale of Impact on Student Loan Borrowers

A Policy Shift: From Pause to Pressure

Collection activity on federal student loans had been largely paused since March 2020 (nbcnews.com). This hiatus provided a much-needed reprieve for millions of borrowers struggling with economic uncertainty. The U.S. Education Department had not collected on defaulted loans for approximately five years. This period allowed many to stabilize their finances without the immediate threat of garnishment or other aggressive collection tactics.

However, the Trump administration resumed these collection efforts after this roughly five-year hiatus (cnbc.com). This policy reversal signals a clear shift in approach. The administration justifies these collection efforts by stating that borrowers, not taxpayers, must repay their loans. They also emphasize that there will be no mass loan forgiveness (npr.org). The Department of Education explicitly stated, “Student and parent borrowers — not taxpayers — must repay their student loans.” This stance underscores a philosophy that places the full burden of repayment squarely on the individual. It rejects broad-based relief measures.

An important aspect of federal student loans is that there is no statute of limitations (npr.org). A statute of limitations is a law that sets the maximum time after an event within which legal proceedings may be initiated. In the context of federal student loans, this means the government can pursue collection efforts indefinitely. This includes wage garnishment, tax refund offset, and Social Security benefit offset, often without a court order (urban.org). This perpetual liability creates immense pressure for borrowers. It ensures that the debt can follow them throughout their lives, regardless of how much time has passed since they first defaulted.

Federal Student Loan Collection Activity Timeline

Understanding the Loan Landscape: Key Terms and Types

To fully grasp the impact of these policies, it is essential to understand the various types of student loans and repayment options. Income-Driven Repayment (IDR) plans are federal student loan repayment options. They calculate a borrower’s monthly payment based on their income and family size, rather than their loan balance (ticas.org). These plans are designed to make loan payments more affordable and prevent default, especially for borrowers with low incomes relative to their debt. IDR plans offer a “light at the end of the tunnel” by providing a path to loan forgiveness after a certain period of payments (ticas.org).

The Saving on a Valuable Education (SAVE) Plan is a new income-driven repayment plan introduced by the Biden administration. It is designed to lower monthly payments for many borrowers by basing them solely on income and family size. It includes unique benefits such as the subsidization of unpaid interest (bidenwhitehouse.archives.gov). Under the SAVE Plan, monthly payments are based solely on a borrower’s income and family size, ensuring they owe only what they can afford. For low-income borrowers, initial payments under SAVE can even be zero until their income increases (bidenwhitehouse.archives.gov). A key benefit is that unpaid interest is subsidized. This means the principal loan balance does not grow due to accruing interest if payments are too low to cover it (bidenwhitehouse.archives.gov). This plan offers unique benefits that distinguish it from previous IDR plans (studentaid.gov).

Beyond repayment plans, it is important to distinguish between different loan types. Parent PLUS and Grad PLUS loans are federal student loans designed to help cover education expenses not met by other financial aid (urban.org). Parent PLUS loans are available to parents of dependent undergraduate students. Grad PLUS loans are for graduate or professional students. Both loan types are offered by the U.S. Department of Education and require a credit check. Subsidized and unsubsidized loans are both federal student loans, but they differ in how interest accrues. For subsidized loans, the U.S. Department of Education pays the interest while the student is in school at least half-time, during the grace period, and during deferment. For unsubsidized loans, the borrower is responsible for all interest that accrues from the time the loan is disbursed, even while in school. This distinction matters because it affects the total amount a borrower will repay (urban.org).

The Federal Student Loan Portfolio refers to the total amount of outstanding student loan debt held and managed by the U.S. Department of Education (studentaid.gov). Its significance lies in its immense size and its impact on the national economy, government budgets, and the financial well-being of millions of Americans. Student debt has grown to $1.6 trillion in the last five years (nbcnews.com). This massive figure highlights the scale of the challenge facing both borrowers and policymakers. Of the nearly 43 million people who owe money, only a little more than a third have made regular payments (nbcnews.com).

Understanding the SAVE Plan

The Saving on a Valuable Education (SAVE) Plan: A new income-driven repayment plan that lowers monthly payments based solely on income and family size. It includes unique benefits like the subsidization of unpaid interest, preventing loan balances from growing due to interest accrual.

The Disproportionate Burden: Impact on Vulnerable Communities

Millions of Americans are affected by these collection efforts, with a significant number of borrowers in default (cnbc.com). The Treasury Department will send notices to 5.3 million defaulted borrowers. This indicates the vast scope of the problem. Certain groups, such as borrowers of color, women, and low-wage earners, are especially vulnerable to student loan debt (urban.org). This vulnerability stems from systemic inequalities that lead to lower incomes, wealth disparities, and higher borrowing needs. These groups are often disproportionately affected by higher education costs. They face greater challenges in repayment, leading to higher rates of delinquency and default. For example, Black students often borrow more for college and have less family wealth to draw upon, making them more susceptible to the harsh realities of default and garnishment.

The DATA states that Social Security checks may be garnished for student loans. However, recent reports suggest that a pause on Social Security garnishment for federal student loans may remain in place (desifacts.org). This discrepancy indicates an evolving policy landscape regarding the collection of student loan debt from Social Security benefits. This uncertainty adds to the anxiety of many older borrowers who rely on these benefits for their livelihood. Proposed cuts and changes to federal student aid could significantly affect borrowers by reducing access to financial assistance, increasing the cost of education, or altering repayment options (urban.org). For the broader student loan system, such changes could impact default rates, the overall federal student loan portfolio,

ABOUT THE AUTHOR

Darius Spearman has been a professor of Black Studies at San Diego City College since 2007. He is the author of several books, including Between The Color Lines: A History of African Americans on the California Frontier Through 1890. You can visit Darius online at africanelements.org.